Private Equity’s Risk Management:Take-Up Caught in the net of Dodd-Frank, FATCA and other reforms, yet another category of financial firms is bulking up in governance, risk and compliance

The Riverside Company, a private equity fund with $4.6 billion in assets under management and offices on four continents, has felt the impact of a host of new rules and regulations including the Dodd-Frank Act, the Foreign Account Tax Compliance Act (FATCA) and Europe’s Alternative Investment Fund Managers Directive (AIFMD).

Since Dodd-Frank became law in 2010, Riverside has hired a chief compliance officer in the U.S. who reports to its chief financial officer, who also functions as the chief risk officer; hired a European compliance officer to manage evolving AIFMD requirements; and brought on a second law firm to focus exclusively on compliance issues.

Riverside also retained a consulting firm to assist with preparation for Securities and Exchange Commission presence exams, part of an SEC initiative to test newly registered investment advisers,and with a gap analysis to identify any material omissions in compliance policies and procedures.The firm has also produced risk and compliance manuals, documented risk procedures and provided staff training for anti-money-laundering and Foreign Corrupt Practices Act compliance. Data protection and privacy rules outside the U.S. have been addressed, as has the SEC’s April alert on cyber security with a formal information security program and periodic system audits.

“We have spent over $2 million on compliance issues” in the Dodd-Frank era, says Pam Hendrickson, Riverside’s New York-based chief operating officer, to whom CFO/CRO Béla Schwartz reports, and chairman of the global board of the Association for Corporate Growth, a private equity trade group.

The sector as a whole has tightened its focus on operational and regulatory matters, not unlike other types of asset managers, as the SEC and other agencies have put them under scrutiny. There have been calls for private equity firms to be registered as broker-dealers, concerns about conflicts of interest and reports of improper fees and expenses that may shortchange investors. Three of the biggest names in the field – the Blackstone Group, Kohlberg Kravis Roberts and TPG – in August joined three other firms in settling charges that they colluded to drive down the prices of takeover targets.

Maturity and Institutionalization

“Legal and compliance is our fastest growing part of the firm by far,” Blackstone Group president and COO Tony James acknowledged to Bloomberg News in May. “We’ve been dealing with this for a long, long time. It’s just there’s more and more and more of it, in more and more jurisdictions,” particularly as the larger firms have expanded internationally.

At the Riverside Company, the CFO/CRO reports to chief operating officer Pam Hendrickson.

Robert Iommazzo, managing partner and head of the risk and compliance practice of executive search firm SEBA International,points out, “As private equity continues to mature as a business, it is becoming more institutionalized,” and as a result, at the larger, global and publicly-held firms, there is a definite appetite for senior risk talent.

At KKR, which has more than $100 billion under management, Attilio Meucci, formerly of Kepos Capital and Bloomberg’s quantitative research unit, joined last year as director of business operations and firm-wide CRO. This year Apollo Global Management, which has $168 billion under management, appointed Jasjit Singh as CRO, capital markets. He was previously a senior risk adviser at the firm. Before that, at Lehman Brothers, he managed the North American proprietary structured credit trading book in the principal strategies division.

Observers say that in private equity, compliance is where the real hiring action is. Bruce Karpati joined KKR this year as chief compliance officer. A former national chief of the SEC’s asset management unit, Karpati was most recently CCO of Prudential Investments.

In all areas relating to compliance, recruiter Iommazzo says, “We’re seeing that demand for talent outstrips supply.”

Paul Gibson, a partner at search firm Heidrick & Struggles, agrees that compliance hiring is up at private equity firms. Regarding risk, he notes that it is difficult to structure enterprise risk programs for private equity firms given their large illiquid portfolios. “Add to that the fact that the talent pool of people who genuinely have illiquid-risk-management experience is incredibly small and underdeveloped,” Gibson says, “and that’s why we haven’t seen huge spikes in CRO hiring in private equity.”

Big-Small Divide

Instead, many non-public, medium- to smaller-sized PE firms have focused on growing their legal teams, combining CFO and CRO functions, asking COOs to do more, and turning to outside consultants for compliance support and help with regulatory-exam preparation.

“We see the larger firms hiring chief compliance officers, while others are asking CFOs to wear more hats and focus more on compliance,” observes Norman Leben, managing principal at GEN II Fund Services, which specializes in private equity fund administration and related services. “Others are leaning more on their law firms or in-house lawyers to help in setting up written risk policies and procedures.”

Scott Gluck, a Washington, D.C.-based attorney with Venable who works with middle-market PE funds, is seeing more use of consultants for compliance functions and manual-writing. “Because middle-market funds don’t have the resources of the larger funds, it is more difficult for them to be compliant, and it’s very costly,” Gluck says.

Danielle Ryea, a senior manager with EY who has an SEC background, says mock SEC exams and audits provided by her firm help PE clients by “highlighting areas where they can make improvements.”

A complication facing private equity, says Guy Talarico, founder and CEO of Alaric Compliance Services, is that “many of these rules were designed for traditional managers that invest in publicly traded equities. The way PE funds operate, they do not fit the regulatory mold.” Assisting with these matters, New York-based Alaric finds that “25% of our new business is now private equity firms. Three years ago, it was zero.”

Source: Adveq/Coller Institute of Private Equity survey of general partners

Established Discipline

When it comes to active risk management – identifying, analyzing and mitigating risk – there are differing perspectives as to the degree to which it has evolved in private equity. Some say that in contrast to compliance, risk has always been a key focus and there is little or no need for much change.

“The big risks for private equity firms are failing to make a successful buyout investment at an attractive price and not performing well for their investors,” says Colin Blaydon, professor of management and director of the Center for Private Equity & Entrepreneurship at Dartmouth College’s Tuck School of Business. Prices paid for buyout deals, what happens if the economy changes or shifts dramatically, and attendant liquidity issues are key risk factors.

Ultimately, Blaydon says, risk management in private equity is all about due diligence, managing the cash pressures that can accompany debt structures, and deal execution. As he sees it, “To date, they have been doing extraordinarily well in managing risks.”

Other observers contend that new regulations, as currently formulated, do not take private equity’s unique characteristics and investment challenges into account and do not raise the industry’s risk management standards.

Brynn Peltz, a New York-based partner with law firm Goodwin Procter, says new regulations have been “a very difficult adjustment for many fund managers.” They tend to have long-term client relationships, and now they are being told how to operate or run their business. Also troubling, Peltz says, is the fact that some of the new rules – like those requiring PE firms tocomply with custody rules that are meant for cash or public securities – are “like trying to fit a square peg into a round hole – and don’t make sense to them.”

Still others say that new regulations – AIFMD in particular – are only starting to be fully understood and that there is indeed room for improvement and standardization in risk management practices.

In a survey released in June and sponsored by investment firm Adveq and London Business School’s Coller Institute of Private Equity, 83% of 36 responding general partners ranked risk management as high or very high on their list of concerns when investing. Most of them assigned responsibility for implementing risk management policies to senior professionals.

While only 4% had no form of risk management in place, 98% were unsure of the benefits of increased regulation, 58% said they believe guidelines are unclear, and 89% were concerned about new risks caused by regulation, with AIFMD and FATCA regarded as most problematic.

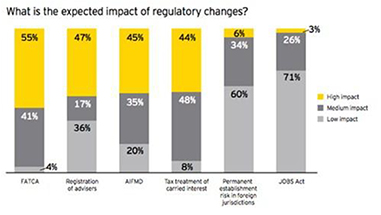

In a first-time survey of chief financial officers in private equity, published this year by EY, 96% deemed FATCA a high- or medium-impact regulatory change, and 80% said the same about AIFMD. The comparable figure for cross-border regulatory risk was 40%, for that related to the U.S. JOBS Act only 29%.

Source: EY survey of private equity CFOs

Competitive Advantage

“If you look at the actual activities at PE funds, and in particular their due diligence practices, risk management is all over the place,” states Lee Gardella, managing director and head of risk management at Adveq, which has $5.7 billion under management and invests in PE funds. However, these activities do not necessarily eliminate the full range of market, operational, legal, accounting and tax risks. The survey concludes by saying that heightened risk management can help PE firms differentiate themselves and gain a competitive advantage.

“Clearly, when it comes to new regulations, we are still at the learning-curve phase,” Gardella says. “Eventually, risk management efforts will become an even more important part of the business and affect the flow of capital.”

According to Samuel Won, founder and managing director of risk advisory firm Global Risk Management Advisors, there is definitely room for risk-management improvement in the private equity world. Practices that could be introduced or expanded upon include: Actively monitoring evolving risks in portfolio companies and in the overall portfolio; looking at how an investment target company’s business has changed or evolved over time; assessing portfolio companies’ enterprise risks; proactively helping to ensure successful exits; and, within the portfolio, analyzing correlations and risk concentrations.

“PE firms could be utilizing risk management to monitor their investments far more closely,” says Won. “They could also be stressing for risks and really screening for the risks in these investments.”

Won predicts that as AIFMD is better understood, it will become a standard by which all funds – in Europe and in the U.S. – will be judged. “In the future, PE funds can use better risk management to make more money, to cover fiduciary risk, and as a differentiator in the marketplace and marketing tool.”

AIFMD’s Effect

Despite “a lot of foot-dragging regarding compliance” – and the occasional blow-up like the $48 billion PE takeover of Texas-based utility TXU Corp. (renamed Energy Future Holdings Corp.), which filed for bankruptcy protection in April – Erik Gordon, a professor at the Stephen M. Ross School of Business, University of Michigan, is upbeat about how risk management is trending in private equity.

Gordon says that thanks to AIFMD – a widespread concern in the above-mentioned EY survey of CFOs – a “decent-sized fund in Europe will have a dedicated risk professional,” though this may not be the case at many U.S. funds that will be relying on consultants and lawyers.

At larger PE funds, risk managers will have opportunities to step up and be more active on the leveraged side of the business.

“PE deal-makers will continue to structure deals and use their judgment on the amount of leverage that is prudent, but I think you will also start to see risk managers, or those in a risk management role, functioning as a second set of eyes, reviewing the deal,” Gordon says. Risk managers will not have veto power, but will provide a second look at the amount of leverage and at the deal structure.

“This is definitely an opportunity area for risk managers,” Gordon adds, noting that the PE industry would clearly benefit, and possibly avoid megadeal debacles, by adopting this approach.

With more and better emphasis on risk, private equity will be looking more like other asset classes in this regard.

“What we are seeing now is private equity catching up with the mutual fund business and other, traditional asset classes in terms of regulation, risk management and the ways they need to conduct business day-to-day,” says Gen II Fund Services’ Leben. “It’s all part of the asset-class maturation process, particularly as the investor base in PE may broaden over time.”

Katherine Heires (mediakat@earthlink.net) is a freelance business and technology journalist and founder of MediaKat llc